Introduction

The pipeline is the most widely used metaphor in sales. It is also one of the most misleading if you happen to work in wealth management.

In a pipeline, a prospect enters at one end, and a client exits at the other. The job of the sales team is to move people forward. It works well enough when the relationship ends at the transaction. Software licenses. Equipment purchases. One-time consulting engagements.

But wealth management is not one of these.

A wealth management relationship does not begin at a pipeline stage and end at a close. It begins with a conversation and, if it works, it lasts decades. The client is not a single contact moving through a sequence. They are one node in a network that includes family, professionals, business interests, and a set of life events that no intake form can fully anticipate.

Most wealth management firms know this intuitively.

The problem is not that firms care too little about client relationships. The problem is that they lack a working model for how relationships actually form in their industry. They default to the only model they have: the linear sales funnel. And that model, applied to wealth management, is like using a road map to navigate the ocean.

Vlad Voskresensky, co-founder of Revenue Grid, sat down with Matt Zeigler, Managing Director at Sunpointe Investments, to talk about what a better model looks like.

They talked about how client relationships form in wealth management, what drives trust within them, where the real data lives, and where technology helps versus where it starts getting in the way

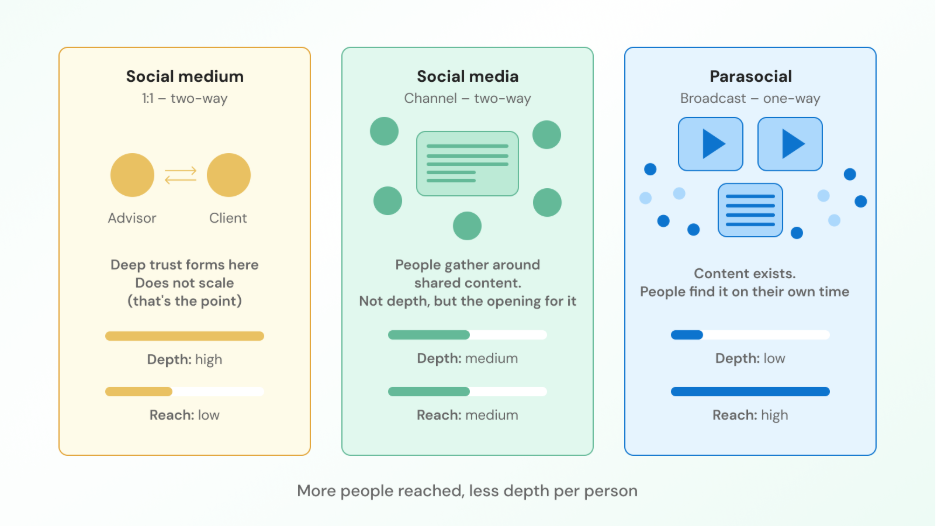

The three layers of client relationship in wealth management firms

The single biggest structural mistake wealth management firms make is treating every client interaction as the same type of engagement. A LinkedIn comment, a planning meeting, and a podcast download are different signals. The result is confusion about what is actually working and why certain efforts refuse to scale.

The fix is a simple taxonomy. There are three layers of relationships, and each one has a

different purpose.

Social Medium: The foundation of trust

This is the singular form of “social media,” and the distinction matters enormously.

A social medium is a two-way conversation between two individuals. Advisor and client, face to face or voice to voice, working through something real. It is the only layer where deep trust actually forms.

It also does not scale. That is the point.

If you try to expand it by cramming more clients into the same calendar or replacing the advisor with a tool, the people already inside that relationship notice immediately.

The social medium is where the advisor earns the right to be trusted with a family’s financial life. Everything else in the firm, the content, the brand, the technology, exists to support this layer or to create the conditions for it to begin.

Social Media: Surface area for discovery

Social media (LinkedIn, a firm’s blog, an industry forum) operates at the channel level, not the individual level. It is also two-way. Someone commented on a post. The advisor responds. A thread develops.

Its job is not depth. Its job is reach.

Social media creates the conditions for a social medium relationship to form, but it is not a substitute for one. The firm that mistakes a thriving LinkedIn presence for thriving client relationships has confused the lobby for the living room.

The Parasocial Layer: Familiarity before conversation

A parasocial relationship is one-way. The advisor broadcasts, the audience listens.

A prospect follows the advisor’s podcast, reads the firm’s newsletter, watches a recorded conversation. No direct interaction has taken place. But over time, the prospect develops a sense of who this advisor is, how they think, and what they stand for.

That familiarity solves one of the hardest problems in wealth management: the referral.

Clients want to refer. But their relationship with their advisor is too personal, too specific to summarize in a sentence. The parasocial layer gives them something to share instead. The prospect arrives at the first meeting already warm, without the advisor spending a single additional minute.

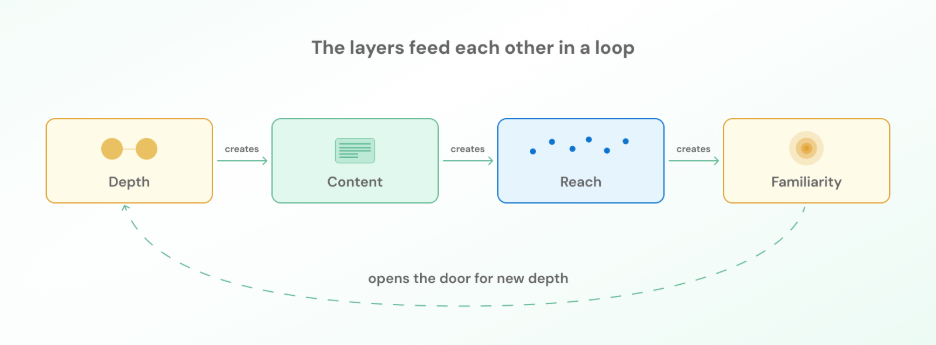

How the layers connect (and where firms confuse them)

These three layers are not isolated from each other. They move in a loop.

A social medium relationship can become a LinkedIn post that reaches hundreds, some of whom follow the advisor’s content, forming parasocial familiarity. One of those followers eventually reaches out, and the cycle returns to social medium.

The three-layer framework tells you where to invest different types of effort. But it does not tell you how trust actually forms inside the layers.

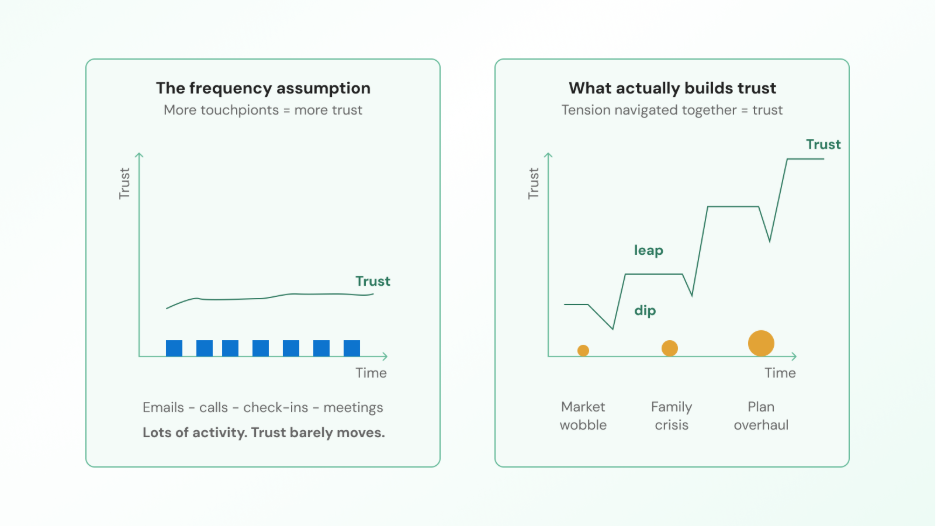

Trust forms through tension, not frequency

The prevailing assumption is that trust scales with frequency. More emails, more check-ins, more meetings. Wealth management exposes how shallow this model is. An advisor can meet a client quarterly for five years and still lose them the first time something goes wrong, if those meetings were never more than pleasant status updates.

What actually builds trust

Trust is the product of navigating difficulty together.

“Trust is always based on a story. It is a mutually understood, shared story. And every story is a function of some tension and resolution.” — Matt Zeigler

Let’s say a client’s child switches from a planned athletic scholarship to musical theater in the spring semester of senior year. The financial plan has to change overnight. The advisor who steps in and works through the new reality alongside the client earns a kind of trust no quarterly review can match.

Zeigler calls this “garden glove service,” a deliberate rejection of “white glove service.”

White gloves are pristine and performative. Garden gloves get dirty on purpose. You put them on when something needs to grow, not just maintaining.

“I don’t want to be your butler. I don’t want the presumption to be; you tell me to go fetch something, and I show up with orange juice on a tray. No white glove service. Not doing it. What I preach is the garden glove service. We’re not afraid to get our hands dirty. Get them dirty in the name of growth. Get into that mud, get into that tension to grow something with your clients.” — Matt Zeigler

The advisor’s job is not to create tension. It is to be ready when it arrives, and to move through it alongside the client rather than retreating behind a standard workflow.

But are firms tracking these moments of tension? In almost every case, the answer is no. Because the tools they rely on were never designed to capture what matters

What gets measured vs. what matters

Consider the mismatch between what most CRMs track and what actually moves a client relationship forward:

| What gets logged | What actually builds trust |

| Calls made | A hard conversation about an aging parent’s care costs |

| Emails sent | A sudden liquidity event that reshapes the family’s financial posture |

| Meetings held | A market downturn that tests whether the advisor panics or stays steady |

Consider the mismatch between what most CRMs track and what actually moves a client relationship forward: None of the right-hand columns show up in an activity dashboard. All of it is where trust either deepens or dissolves.

How do you know if a firm is a confusing process with a relationship?

The barbecue book test

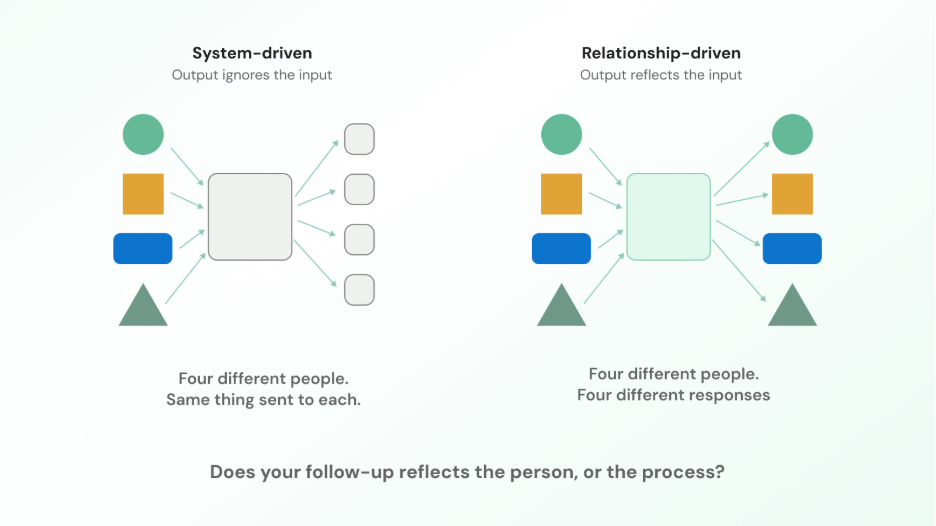

There is a simple way to tell whether a firm is building relationships or running a system that looks like one.

Ask: does the thing we send, say, or do after meeting a prospect reflect something specific about that person? Or would it be exactly the same regardless of who sat across the table?

Zeigler encountered this test early in his career. At a conference, a successful advisor revealed his “secret” to converting prospects: he sent every single one of them a book about barbecue. The same book. Every prospect.

This relationship strategy scales. But it is also completely disconnected from the person receiving it. The advisor who sends a vegetarian a book about smoking brisket has revealed something important: the system, not the client, is running the show.

If trust is built through tension and resolution, then the question becomes: where does evidence of those moments live inside a firm? It definitely does not live in a CRM or activity log. The tensions that build trust in wealth management are life events, family shifts, and financial disruptions.

The data that matters lives on the service side

Every wealth management firm runs two processes in parallel. There is a sales process and a service process. Most firms have instrumented the first one thoroughly and left the second one living inside the advisor’s head. That split is where the blind spot begins.

Two parallel processes, one instrumented

The sales process tracks what most dashboards measure: new accounts opened, AUM onboarded, revenue per advisor, attrition rates. These metrics matter for the business. They tell you almost nothing about the health of the client relationship.

The service process has data that is hardest to capture, because so much of it is unstructured: family circumstances, life events, shifting priorities, dependencies that evolve over years.

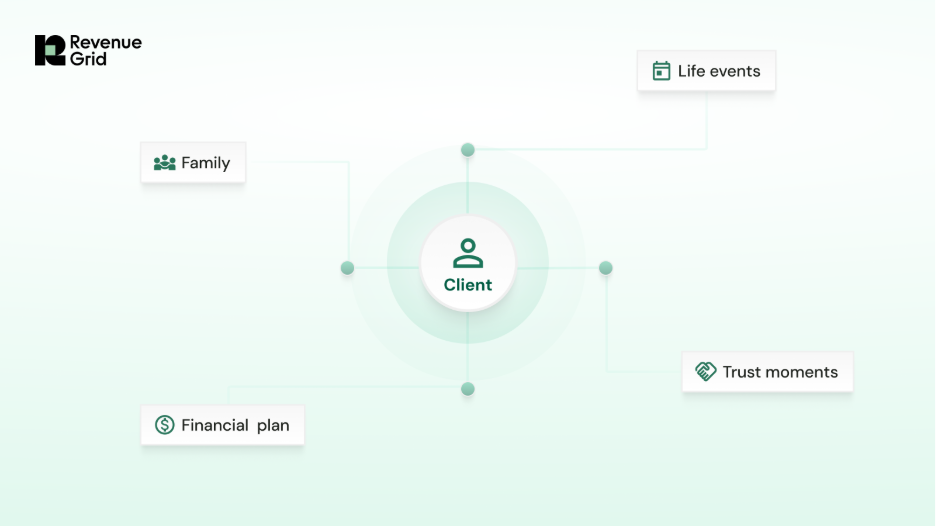

In wealth management, this unstructured data lives inside the financial plan.

What the financial plan actually contains

A financial plan, when used well, is not a document filed at onboarding and forgotten. It is a living map of the client’s world:

- The team. Every person the client is financially and psychologically responsible for.

- The calendar. Known future events: college, mortgage payoff, retirement target, business sale, planned gift.

- The cash flows. Money in and money out, from tax payments to 401(k) contributions.

- The balance sheet. What they own and what they owe, and how it’s structured.

- The contingencies. What happens if someone lives longer than expected, dies earlier, gets sick, or gets sued.

This is the data that captures the context around trust-building moments.

If this data exists, a firm with 300 client households and complete financial plans can answer questions like these with precision:

“How many clients are approaching Medicare eligibility in the next twelve months?”

“Which households have children starting college this fall?”

“How many clients are preparing a liquidity event in the next two years?”

A firm that can answer those questions is embedded in its clients’ lives in a way that makes retention almost automatic

But a firm is not a single relationship.

At some point, every wealth management firm faces the question of how to multiply what’s working without destroying it. And this is where the logic of wealth management relationships gets most counterintuitive, because the answer is not to scale the relationship itself.

Scenes and startups: Knowing which parts of your firm can grow

Think about any community that worked because of its size. A close-knit professional group. A small advisory firm where every client knows the founder by name. The value comes from the fact that everyone in the room has a relationship with everyone else. That is what makes it a scene.

In wealth management…

Scene cannot scale

The advisor-client relationship is personal, bespoke, and built on shared context. An advisor can build a thriving practice with 80 to 100 of these relationships. That is not a limitation. That is the model.

“The moment you try to scale something that worked because it was small and personal, it falls apart. The people who were there first notice immediately. They liked it because of the attention, the detail, and the feeling that someone actually knew them. You take that away, and you’ve made it weird.” — Matt Zeigler

But the advisor relationship is not the only part of the firm. And the parts that sit around it operate on completely different logic.

What can scale: The brand, content, & reach

A firm’s brand, its content, its inbound funnel, its parasocial presence across podcasts and newsletters and social channels, all of this is scalable.

Zeigler calls them the startup side of the business. Not a startup in the venture-backed sense. A startup in the sense that it is built to grow.

These are the parts of the business that are built to reach people the advisor has never spoken to and create conditions for future relationships to begin. Unlike the scene, these systems get better with volume, not worse. More listeners, more readers, more followers mean more surface area for new relationships to form.

Both sides of the firm, the scene and the startup, need tools to operate well. But they need them in different ways. And the firms that get into trouble are usually the ones that let a tool built for scale creep into the part of the business that was never meant to scale.

Where tools help and where they get in the way

The principle is simple: tools should catalog, prepare, and support the advisor. They should never sit between the advisor and the client at the moments where trust is formed.

Where tools earn their place

Behind the social medium layer, the right tools make the advisor better at the job that only the advisor can do.

It can be financial planning software that aggregates balance sheets across custodial relationships. AI that summarizes unstructured client data and flags upcoming life events across hundreds of households. Or a CRM system that ensures everyone on a service team can find the right information without relying on the lead advisor’s memory.

Where tools erode trust

The moment a tool starts handling the parts of the relationship that require a human, trust fades.

For example, when an AI sends a pitch email. When an automated sequence handles the follow-up after a difficult meeting. When a chatbot fields the first response to a client who just lost a parent.

“The biggest differentiator of a story you can tell right now, to tell a friend about, is like, oh, my person just picks up the phone. Or I could text them right now, and they’ll text me right back.” — Matt Zeigler

In a world drowning in automated outreach, the simplest act of presence has become a competitive advantage.

But in wealth management, where client data is sensitive and regulation is tight, which tools you use matter just as much as where you use them.

The compliance question

For firms in regulated industries, they must think about what client data is acceptable to feed into an AI tool? What is a secure, vetted platform? Where is the line between a tool that enhances the service process and one that introduces regulatory risk?

These boundaries need three things:

- A written AI policy statement, reviewed by legal counsel.

- Clear distinction between approved tools (SOC 2 compliant, purpose-built) and general-purpose platforms (where client data should never go).

- Team-wide understanding of where the lines are drawn.

The firms getting this right are not avoiding AI. They are using it aggressively behind the relationship and keeping it strictly out of the social medium layer.

The bottom line

Every trend in wealth management right now points toward automation, scale, and efficiency. Most of those trends are right. For the brand, the content, the reach, the infrastructure behind the advisor, scale is the correct instinct.

But the core of a wealth management firm is still one advisor and one client, sitting across from each other, working through something that matters. That part has not changed. It will not change because someone buys better software.

The firms that do well from here will be the ones that can hold both ideas at once. Scale everything around the relationship. Protect the relationship from the scaling.